Section 59 E 2 Expenditures

Pin On Homes Advice Property News Articles

How And Why Pet Ownership Costs Continue To Rise With Images Pet Grooming Business Natural Dog Care Pet Grooming

Knowledge Base Solution How Do I Enter Section 59 E 2 Expenditures From Passthrough Activities Into A 1040 Return Using Worksheet View

87 Of Enterprises Believe Big Data Analytics Will Redefine The Competitive Landscape Of Their Industri Big Data Analytics Data Analytics Data Driven Marketing

19 Likes 2 Comments Jessica Bujo In Madness On Instagram January S Expenses And S Bullet Journal Expenses Bullet Journal Savings Finance Bullet Journal

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqw4iteivaqdctosn5jelnes2a7kp5u Wt0rw Usqp Cau

Section 59 e 2 expenditures on an attached statement the partnership will show the type and the amount of qualified expenditures for which you may make a section 59 e election.

Section 59 e 2 expenditures. In the case of any taxable year of a corporation described in subparagraph c of section 59 a 2 of the internal revenue code of 1986 as added by paragraph 1 which begins after december 31 1989 and includes march 31 1990 the amount determined under. The statement will also identify the property for which the expenditures were paid or incurred. To amortize section 59 e 2 expenditures instead of deducting the entire expenditure in the current year enter the total amount as an amortizable asset on the fixed asset form.

To enter 59 e 2 expenditures do the following. Go to section 3 activity continued. The statement will also identify the property for which the expenditures were paid or incurred.

These expenses flow to their own line on the schedule e page 2 below the passthrough entity that it. On an attached statement the partnership will show the type and the amount of qualified. In line 1 j section 59 e 2 expenditures enter the appropriate data.

On an attached statement the partnership will show the type and the amount of qualified expenditures for which you may make a section 59 e election. Choose the appropriate subcategory associate the asset with the k 1 activity. Section 59 e allows any qualified expenditure to which an election under section 59 e applies to be deducted ratably over the 10 year period 3 year period in the case of circulation expenditures described in section 173 beginning with the taxable year in which the expenditure was made or in the case of intangible drilling and development costs deductible under section 263.

On an attached statement the partnership will show the type and the amount of qualified expenditures for which you may make a section 59 e election. 59 e 2 qualified expenditure. Line 13j section 59 e 2 expenditures amounts reported in box 13 code j represent a taxpayer s share of qualified expenditures that the taxpayer may make a section 59 e election for.

The partnership should provide the taxpayer with a statement that identifies the property or properties for which the expenditures were incurred or paid. Plr 107660 12 2 section 59 e 2 includes in the definition of qualified expenditure any amount which but for an election under 59 e would have been allowable as a deduction for the taxable year in which paid or incurred under 174 a relating to research and experimental expenditures. The statement will also identify the property for which the expenditures were paid or incurred.

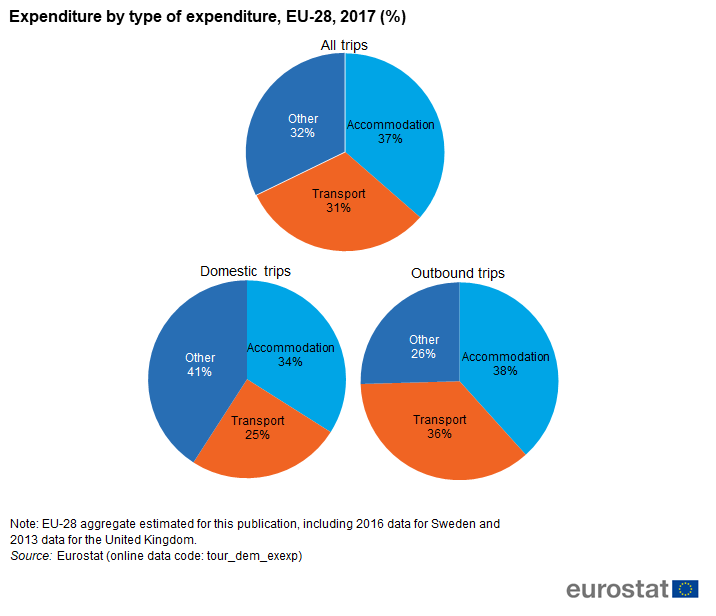

Tourism Statistics Expenditure Statistics Explained

Business Proposal Format Template Fresh Business Proposal Template Excel Xlts In 2020 Business Proposal Format Proposal Templates Business Proposal

Pin By Daliah Gonzalez On Aesthetic Ll In 2020 Law Of Demand Essay Marginal Utility

Why Your Medical Bills Are So High And How To Lower Them Infographic Infographic Health Medical Billing Healthcare Costs

Lilyliseno Com Nbspthis Website Is For Sale Nbsplilyliseno Resources And Information Expense Tracker Excel Expense Tracker Excel Templates

Pin On Education Statistics

Fakta A Cisla Jak Vypada Novy Parlament

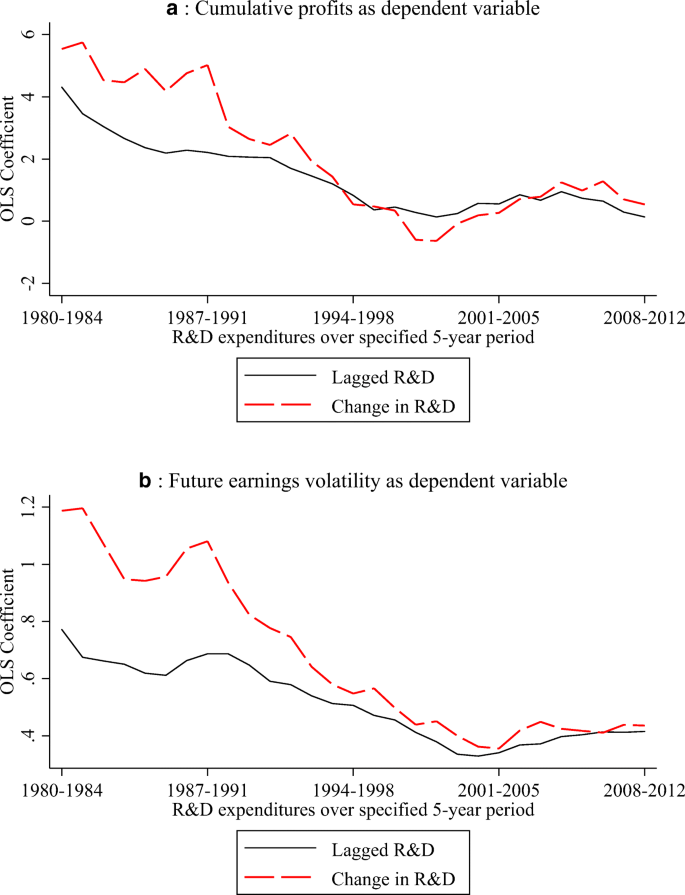

The Changing Implications Of Research And Development Expenditures For Future Profitability Springerlink

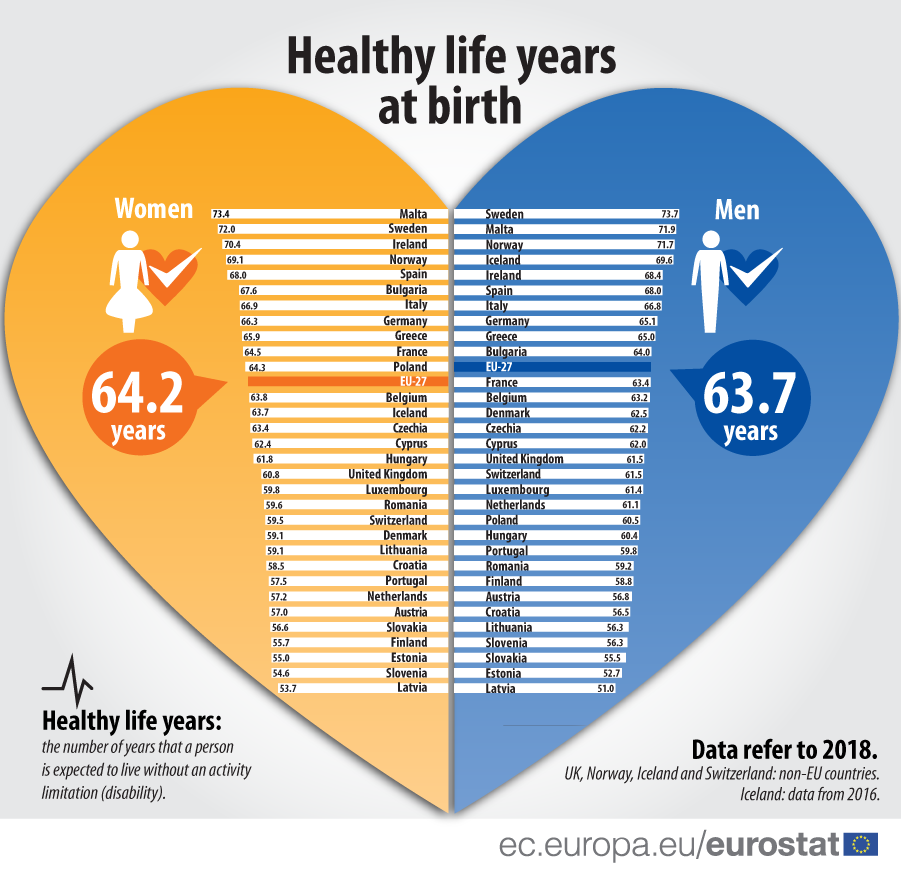

Healthy Life Years Statistics Statistics Explained

Social Media How Engaged Is Your Brand Infographic Social Media Social Media Marketing Social Media Engagement

Free Download Inventory Value Stock Excel Spreadsheet Sample Spreadsheet Business Inventory Organization Excel Spreadsheets

Japan S About Face Data Global Military Expenditures Wide Angle Pbs

What Are Consumers Looking For From An In Store Shopping Experience Marketing Data Infographic Marketing Turn Ons