Section 1245 Recapture

Section 1245 Depreciation Recapture Income Tax Course Cpa Exam Regulation Tax Cuts And Jobs Act Youtube

Section 1245 And 1250 Recapture Provisions Youtube

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

Ppt Ch 17

Solved Section 1245 Recapture Rule Lo 8 Maria Sells Th Chegg Com

Solved Capital Gains And Losses Section 1245 Recapture R Chegg Com

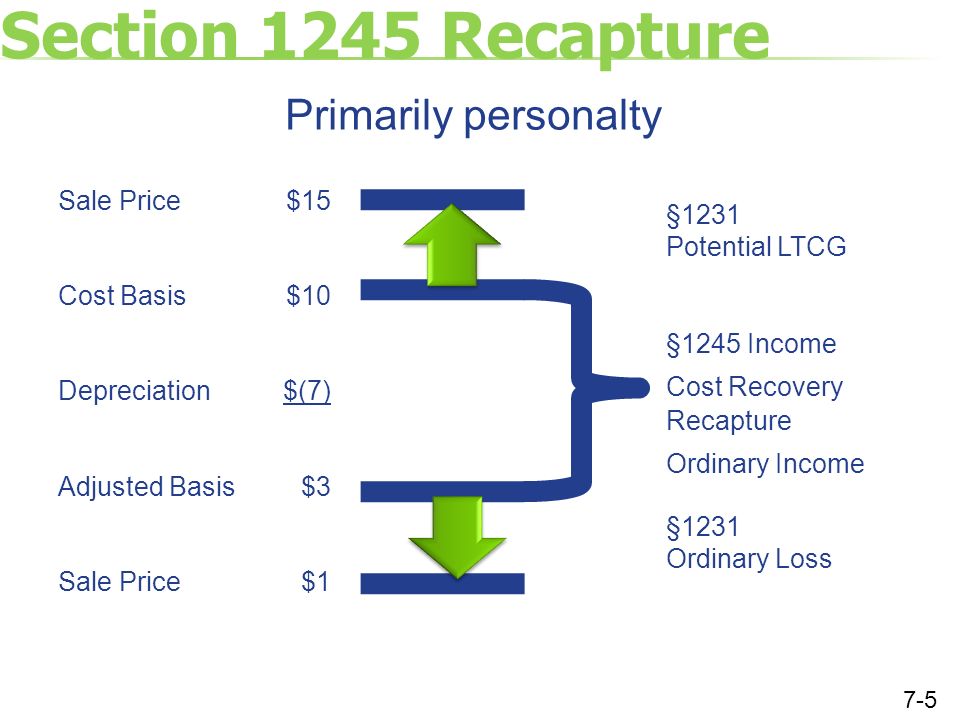

The first step in evaluating depreciation recapture is to determine the cost basis of the asset.

Section 1245 recapture. Section 1245 depreciation recapture. The original cost basis is the price that was paid to acquire. Recapture these two parts are taxed differently resulting in extra taxes.

This type of property includes tangible personal property such as furniture and equipment that is subject to depreciation or intangible personal property such as a patent or license that is subject to amortization. 1245 and 1250 property are not treated the same in recapture in the case of 1250 property only accelerated depreciation taken in excess of straight line depreciation is considered ie for land improvements all accelerated deprecation 1245 or 1250 is recaptured at ordinary rates currently 37 for individuals 25. The part of the gain that is due to depreciation recapture is treated as ordinary income.

Ordinary income is typically taxed at a higher income tax rate than long term gains would be. Facility for bulk storage of fungible commodities. The internal revenue code includes multiple classifications for property.

99 514 201 d 11 b amended par. Gain treated as ordinary income. Bloomberg tax portfolio depreciation recapture sections 1245 and 1250 no.

All three of the following must be true in order for depreciation recapture to occur. Sections 1245 and 1250 were enacted to close the loophole that resulted from allowing depreciation deductions on assets to offset ordinary income while taxing gain from the sale of these. Avoiding depreciation recapture on section 1245 property.

2 generally restating former subpars. Buildings and structural components. Section 1245 property defined.

Solved Section 1245 Recapture Rule Unrecaptured Section Chegg Com

Capital Gains And Losses Section 1245 Recapture R Chegg Com

Solved Capital Gains And Losses Section 1245 Recapture R Chegg Com

Solved Section 1245 Recapture Rule Lo 8 Avalon Inc Chegg Com

Session 7 Sales Of Business Assets Ppt Video Online Download

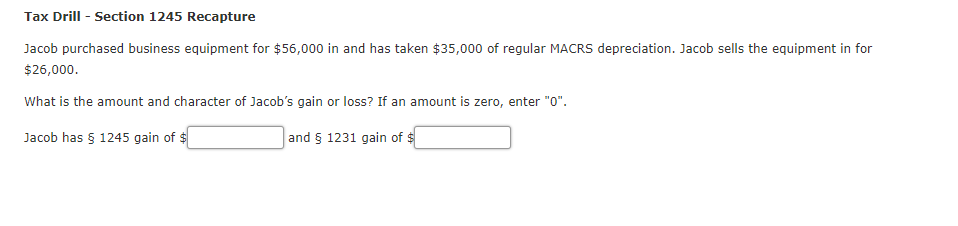

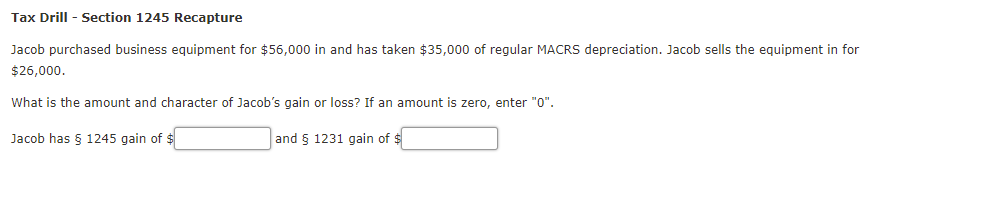

Solved Tax Drill Section 1245 Recapture Jacob Purchased Chegg Com

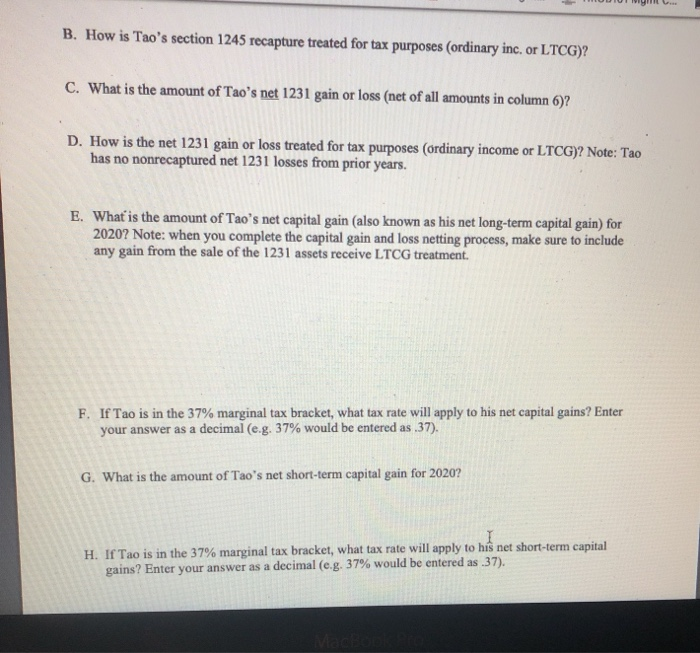

Solved Auw B How Is Tao S Section 1245 Recapture Treated Chegg Com

Section 1245 Depreciation Recapture Income Tax Course Cpa Exam Regulation Tax Cuts And Jobs Act Youtube

Section 1245 Depreciation And Amortization Recapture Youtube

Solved Tax Drill Section 1245 Recapture Jacob Purchased B Chegg Com

Section 1245 Assets Corporate Income Tax Cpa Reg Ch 14 P 5 Youtube

1231 1245 And 1250 Property Used In A Trade Or Business

Solved Question 33 Section 1245 Depreciation Recapture Ap Chegg Com