Irc Section 125

Cafeteria Plan Wikipedia

Hr Help Benefits Help Not Getting The Service You Should At Your Current Peo Concurrent Hro Has Got Your Back Contact Energy Healing Biohacking Nootropics

How An Hsa Works With A Section 125 Cafeteria Plan By Aaron Benway Cfp Ea Medium

What Is A Section 125 Plan And Who Needs One Onedigital

Minimal Handrail Bracket Handrail Brackets Handrail Dining Area Design

Wall Bracing And The Irc Wall Wall Panels Online Frames

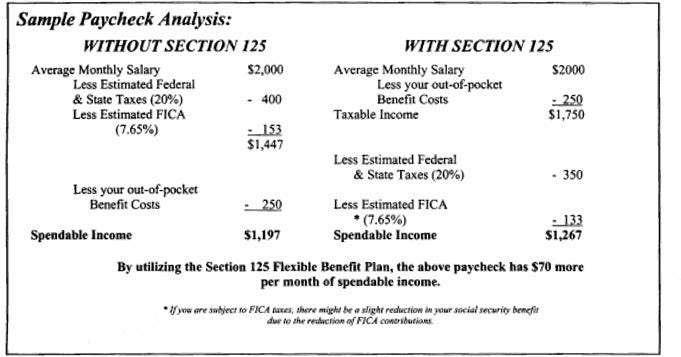

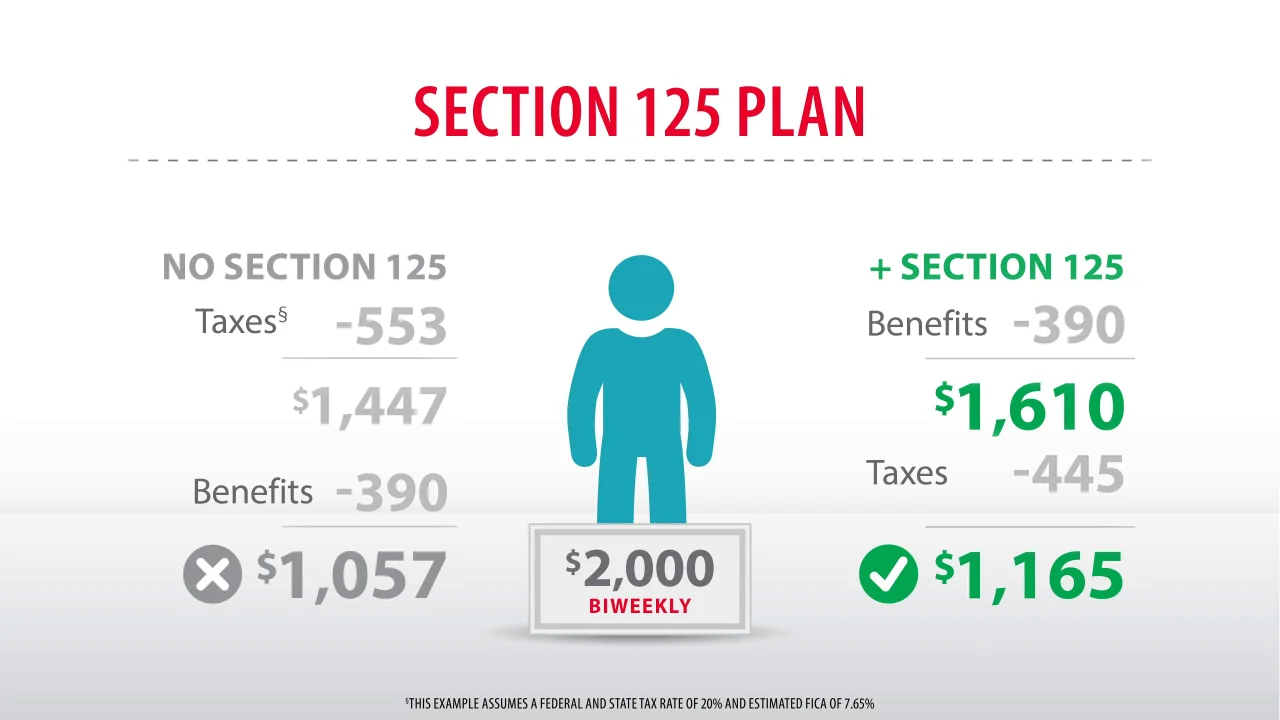

Cafeteria plans include both taxable and nontaxable benefits.

Irc section 125. Some of the. For provision that for purposes of section 125 of the internal revenue code of 1986 a plan shall not be treated as failing to be a cafeteria plan solely because under the plan a participant elected before january 1 1988 to receive reimbursement under the plan for dependent care assistance for periods after december 31 1987 and such. Irs section 125 code cafeteria plan documents are one of the most underused employee benefits for small businesses.

A cafeteria plan is a type of employee benefit plan offered in the united states pursuant to section 125 of the internal revenue code. The plan is called a cafeteria plan because it includes a menu of benefits for employees to choose from. Section 125 of the internal revenue code defines rules that allow employers to offer cafeteria style benefit plans to their employees according to the irs.

Section 125 f defines a qualified benefit as any benefit which with the application of 125 a is not includable in the gross income of the employee by reason of an express provision of chapter i of the internal revenue code other than 106 b 117 127 or l32. For provision that for purposes of section 125 of the internal revenue code of 1986 a plan shall not be treated as failing to be a cafeteria plan solely because under the plan a participant elected before january 1 1988 to receive reimbursement under the plan for dependent care assistance for periods after december 31 1987 and such. It provides participants an opportunity to receive certain benefits on a pretax basis.

Irs section 125 tax code. Its name comes from the earliest such plans that allowed employees to choose between different types of benefits similar to the ability of a customer to choose among available items in a cafeteria qualified cafeteria plans are excluded from gross income. A cafeteria plan is a separate written plan maintained by an employer for employees that meets the specific requirements of and regulations of section 125 of the internal revenue code.

Section 125 of the internal revenue code refers to cafeteria plan benefits. These plans allow employees to pay tax free premiums for group health insurance and other qualified benefits such as group term life accident long term care and dread disease coverage medical expenses and dependent care expenses. These benefits may be.

22 1986 an employee elects under a cafeteria plan under section 125 of the internal revenue code of 1986 coverage for group legal benefits to which former section 120 of such code applies such election may at the election of the taxpayer apply to all legal services provided during 1986.

What Is A Section 125 Pop Premium Only Plan Gusto

New Irs Guidance Provides Employers With Section 125 Plan Flexibility During 2020

Examples Of Financial Goals By Age Groups

Section 125 Plan Administration American Fidelity

Maya Angelou Is Coming To Houston Daily Dish Dish Houston International Day Of Peace Houston Maya Angelou

Loft House First Floor Plan With One Bedroom Loft House Design Loft House Small House Catalog

3zenajpp6 Clrm

Irs Section 125core Documents

Surefire M900v Bk Wh Vertical Foregrip Incandescent Weaponlight With Ir Navigation Leds Throw Lever Mount 1 62 Bezel 125 Or 225 Lumens Flashlight Armas

Seccion De Cubierta Onahus

Http Doa Alaska Gov Drb Pdf Employer Cafeteriaplans Slidesnoteshandout Pdf

Little Tikes 19178 Little Tikes Rc Wheelz First Racers Radio Controlled Truck Buy It Now Only 28 61 On Eba New Trucks Remote Control Trucks Little Tikes

Cobranotice Net Simplify Your Administrative Tasks For Federal And State Cobra Notices