Section 179 Rental Property

Understanding Depreciation Recapture When You Sell A Rental Property In 2020 Estate Tax Rental Property Capital Gains Tax

New Investment Property Calculator Excel Spreadsheet Xlstemplate Xlssample Xls Investment Property Rental Property Investment Investment Property For Sale

How The New Tax Law Affects Rental Real Estate Owners

How Bonus Depreciation Affects Rental Properties Millionacres

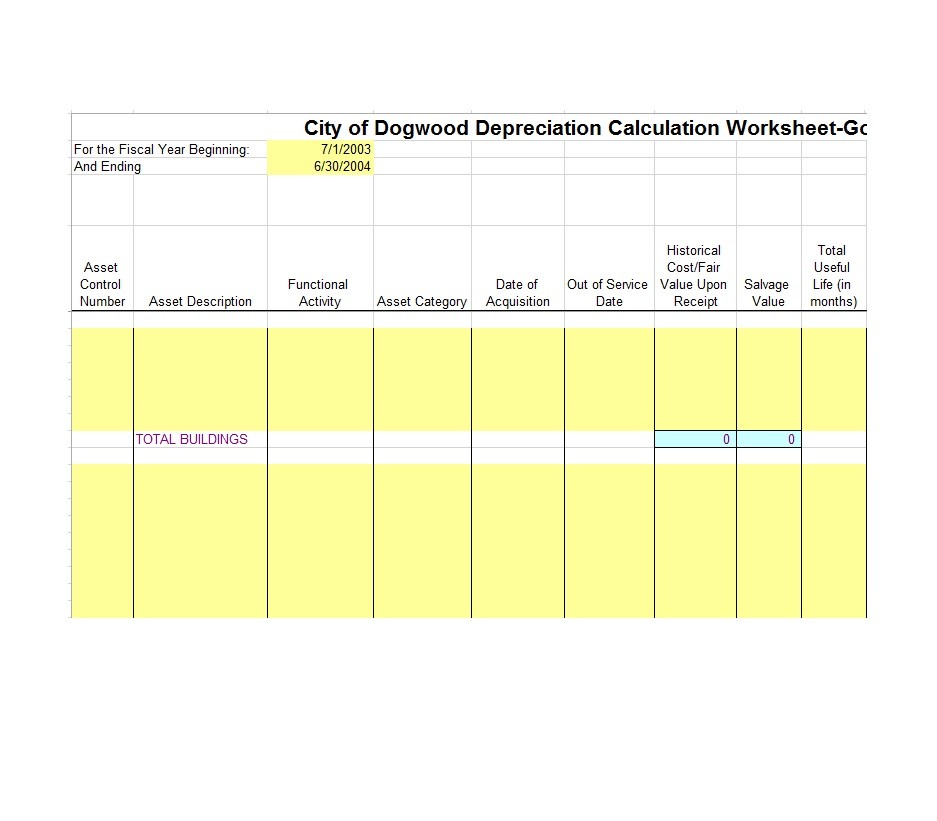

35 Depreciation Schedule Templates For Rental Property Car Asserts

Rental Property Spreadsheet Template For 25 Properties Business Rental Property Management Property Management Marketing Being A Landlord

However the tax cuts and jobs act eliminated this restriction starting in 2018.

Section 179 rental property. A frequent question asked by tax professionals is whether home furnishings such as washers dryers refrigerators microwaves and the like used as part of a residential rental qualify for the section 179 expense deduction. Unfortunately section 179 does not apply to real property. Yes while you cannot take section 179 deduction for the residential rental property itself you can use section 179 to deduct tangible long term personal property.

See chapter 2 of pub. It is separate from your depreciation deduction. In the past section 179 could not be used to deduct personal property used in residential rental property.

946 for more information about claiming this deduction. Liberalized section 179 deduction rules. Section 179 allows taxpayers to deduct the cost of certain property as an expense when the property is placed in service.

179 generally applies to sec. The recapture period for real property has not changed through section 179. Okay i figured out the problem.

The section 179 deduction is a means of recovering part or all of the cost of certain qualifying property in the year you place the property in service. Section 179 is for purchases that are used for the active conduct of the taxpayer s trade or business and is limited by the total trade or business income however rentals are not always a trade or business. For qualifying property placed in service in tax years beginning after december 31 2017 the tcja increases the maximum section 179 deduction to 1 million up from 510 000 for tax years beginning in 2017.

This includes for example kitchen appliances carpets drapes or blinds. Qualified leasehold improvement property qualified restaurant property and qualified retail improvement property are allowed a section 179 deduction even if the properties relate to a schedule e rental property as long as the lessor considers the rental an active trade or business. The phase out limit increased from 2 million to 2 5 million.

Property Management Excel Spreadsheet Rental Property Investment Property Rental Property Management

Tenant Payment Ledger Remaining Balance Rent Due Calculator 25 Properties Rental Property Management Rental Property Rental Income

Landlord Rental Income And Expenses Tracking Spreadsheet 5 80 Properties Rental Property Management Being A Landlord Property Management

Rental Property Management Template Long Term Rentals Rental Income And Expense Categories Rental Property Management Rental Income Rental Property

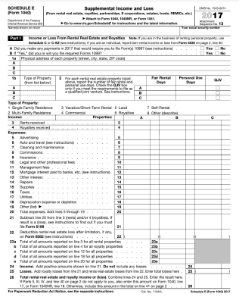

4562 Listed Property Type 4562

:max_bytes(150000):strip_icc()/GettyImages-1056502202-b3fba961eb6c42b68fe6bf0c68bc977f.jpg)

Listed Property Definition

5 Free Rental Property Expenses Spreadsheets Excel Tmp In 2020 Rental Property Rental Property Management Being A Landlord

Rental Property Depreciation Rules Schedule Recapture

Marketing And Social Media Planner Social Media Printable Etsy Business Planner Printable Planner Planner

Landlords Spreadsheet Template Rent And Expenses Spreadsheet Etsy Being A Landlord Spreadsheet Template Rental Property Management

Irs Issues Guidance For Change To Real Property Depreciation Grant Thornton

Optimizing Residential Real Estate Deductions Journal Of Accountancy

What Is Section 179 How Can It Benefit You Millionacres