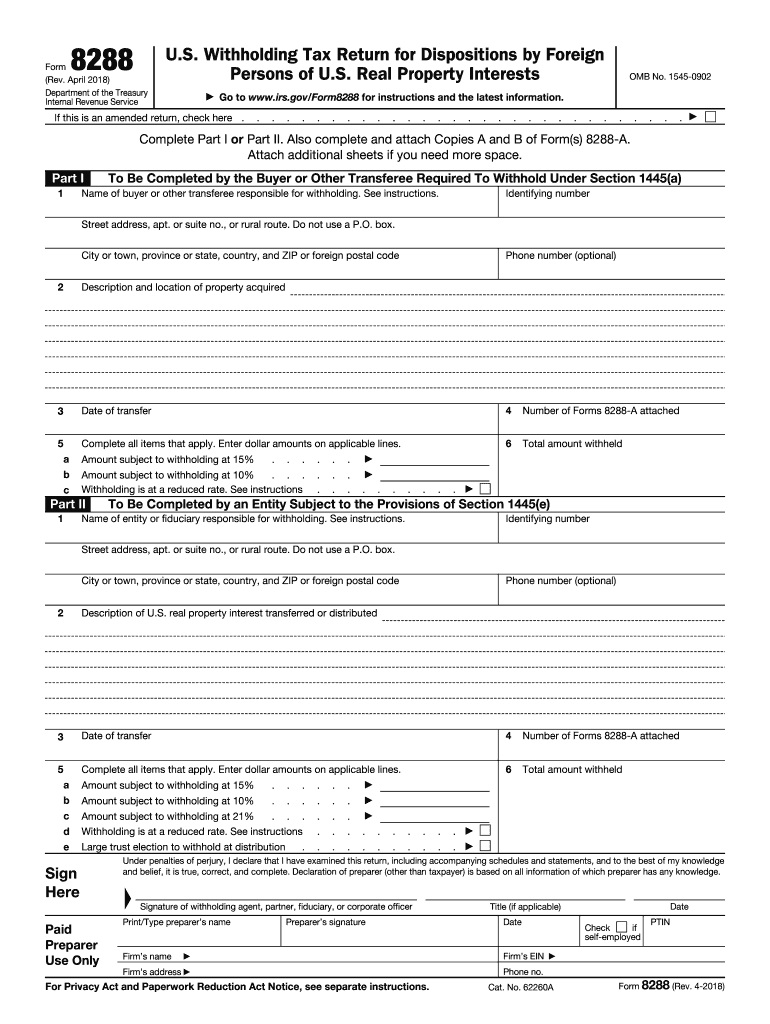

Section 1445 Of The Internal Revenue Code

3 21 261 Foreign Investment In Real Property Tax Act Firpta Internal Revenue Service

3 22 261 Foreign Investment In Real Property Tax Act Firpta Internal Revenue Service

Https Www Illinois Ticortitle Com Services Non Foreign Certification Transferee 20transferor Pdf

Foreign Affidavit Pdf Fill Out And Sign Printable Pdf Template Signnow

Https Nationalagency Fnf Com Portals Dc Training 20resources 2018 20seminar Mark 20bayer Firpta 20presentation Pdf Ver 2018 09 11 162822 137 Timestamp 1536701325206

4 61 12 Foreign Investment In Real Property Tax Act Internal Revenue Service

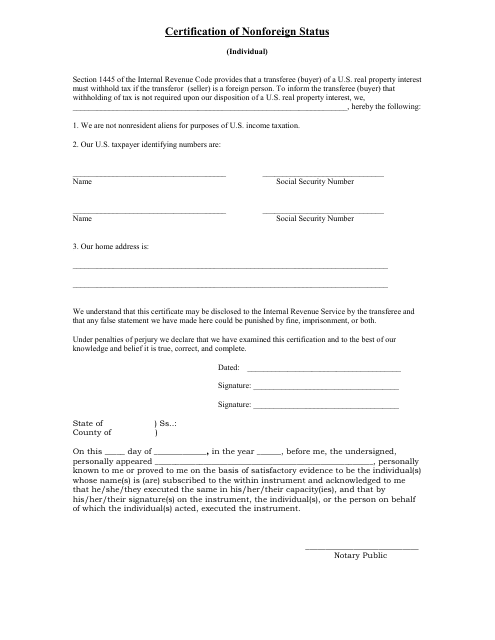

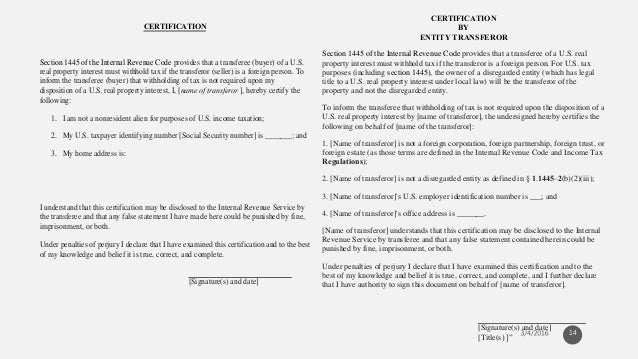

Real property interest must withhold tax if the transferor is a foreign person.

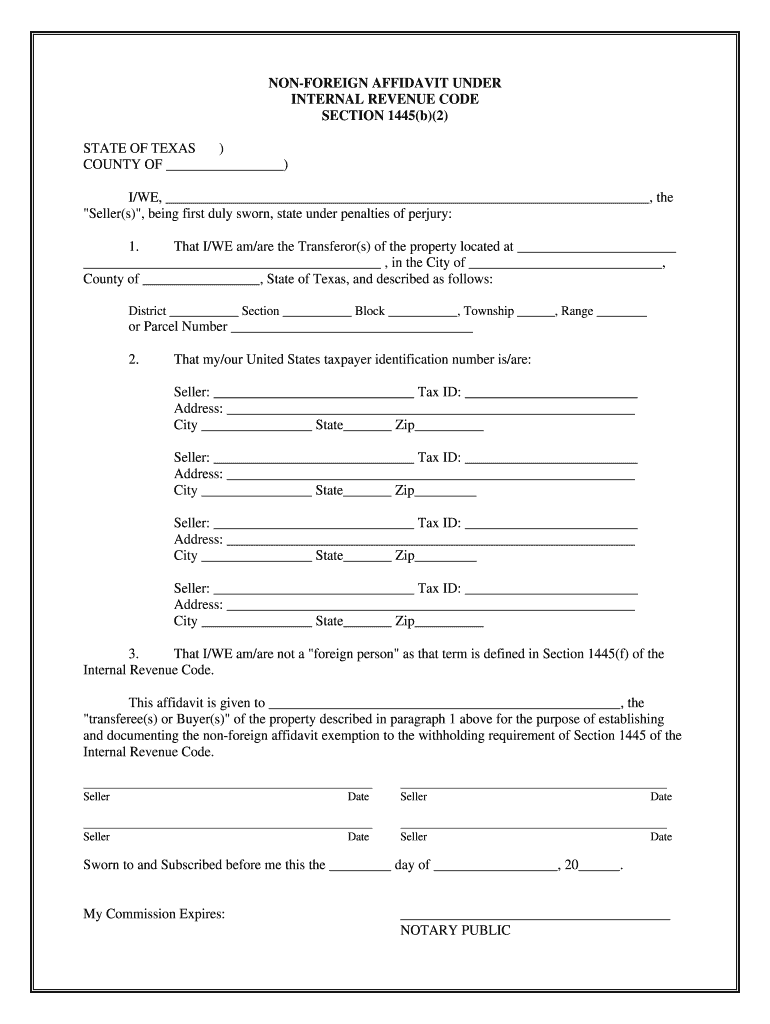

Section 1445 of the internal revenue code. 1445 a general rule except as otherwise provided in this section in the case of any disposition of a united states real property interest as defined in section 897 c by a foreign person the transferee shall be required to deduct and withhold a tax equal to 15 percent of the amount realized on the disposition. Tax purposes including section 1445 the owner of a disregarded entity which has legal title to a u s. Code 1445 withholding of tax on dispositions of united states real property interests.

Section 1445 of the internal revenue code provides that a transferee of a u s. Except as otherwise provided in this section in the case of any disposition of a united states real property interest as defined in section 897 c by a foreign person the transferee shall be required to deduct and withhold a tax equal to 15 percent of the amount realized on the disposition. Real property interest under local law will be the transferor of the property and not the disregarded entity.

Withholding of tax on dispositions of united states real property interests on westlaw findlaw codes are provided courtesy of thomson reuters westlaw the industry leading online legal research system. Real property interest from a foreign person must withhold a tax of 15 percent 10 percent in the case of dispositions described in paragraph b 2 of this section from the amount realized by the transferor foreign person or a lesser amount established by agreement with the internal revenue service. Internal revenue code 1445.

If an nra qualifies to claim the irc 121 exclusion the statutory withholding under irc 1445 on the amount realized from the sale could exceed the maximum tax liability on the sale.

3 22 15 Foreign Partnership Withholding Internal Revenue Service

3 21 15 Foreign Partnership Withholding Internal Revenue Service

Https Www Wra Org Lu1911

Escrow Number Agreement Concerning Firpta Withholding Pdf Free Download

Irs Form 8228b Fill Out And Sign Printable Pdf Template Signnow

Http Investors Johnsoncontrols Com Media Files J Johnson Controls Ir Tax Notification Tyc Usrpi Status Under Section 1 897 2 Pdf

3 8 45 Manual Deposit Process Internal Revenue Service

3 21 110 Processing Form 1042 Withholding Returns Internal Revenue Service

Firpta Certification For Sellers Real Estate Lawyer

Certification Of Nonforeign Status Individual Download Fillable Pdf Templateroller

Firpta Foreign Investment In Real Property Tax Act

2 3 35 Command Code Irptr Internal Revenue Service