Section 1231 Property Definition

/man-working-in-computer-1135595001-31f457ad7db84839938774cea99939e0.jpg)

Section 1231 Property

Square And Cube Root Table Image Collections Table Decoration Ideas Root Table Math Charts Math Formula Chart

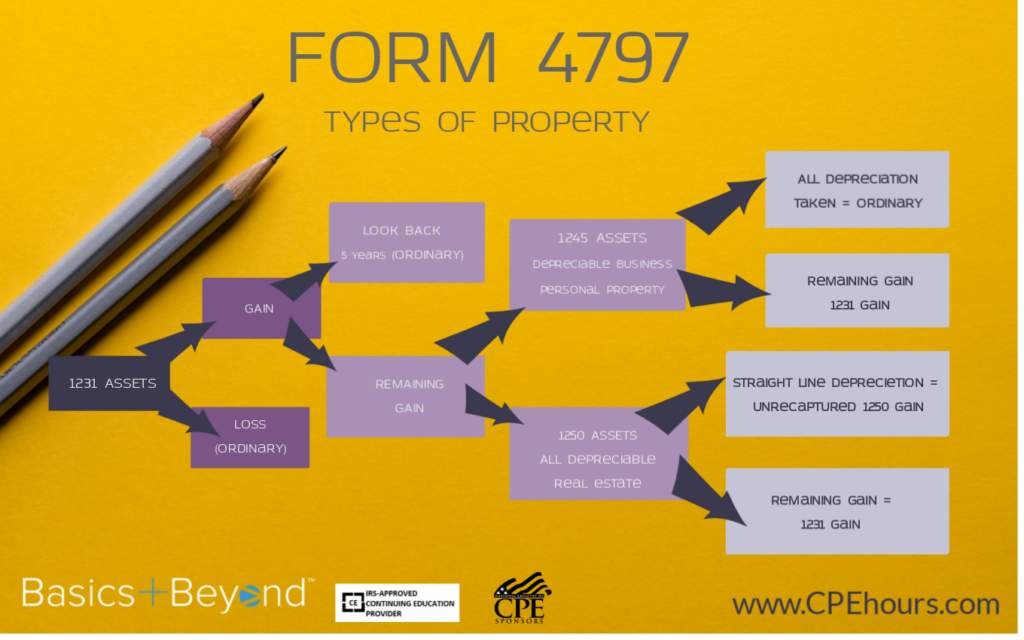

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

Http Investor Apachecorp Com Static Files 92f9e587 Ae4a 4b89 9fcc 33a78f9a7d13

1231 1245 And 1250 Property Used In A Trade Or Business

Plan 62813dj One Bed Post Frame Country Home Plan With Wraparound Porch In 2020 Porch House Plans Country House Plans Pole Barn House Plans

Buildings and equipment used in a trade or business and held for more than one year.

Section 1231 property definition. If section 1231 assets are held for the required period of time capital gain treatment is available for a deductible ordinary loss. The net section 1231 gain for any taxable year shall be treated as ordinary income to the extent such gain does not exceed the non recaptured net section 1231 losses. Generally property held for the production of rents or royalties is considered to be used in a trade or business.

Section 1231 property section 1231 property section 1231 property includes depreciable assets and real estate used in a trade or business and held for more than one year. The following transactions result in gain or loss subject to section 1231 treatment. Sales or exchanges of real property or depreciable personal property.

Learn about 1231 1245 1250 property and its treatment for gains and losses. 1231 1245 and 1250. Under certain circumstances it also includes timber coal domestic iron ore livestock held for draft breeding dairy or sporting purposes and unharvested crops.

1231 property includes depreciable property and real property e g. 2 non recaptured net section 1231 losses for purposes of this subsection the term non recaptured net section 1231 losses means the excess of. This property must be used in a trade or business and held longer than 1 year.

Section 1231 property refers to property used in a trade or business that has depreciable value. Equipment vehicles and rental real estate can be regarded as section 1231 properties. Section 1231 property is real or depreciable business property held for more than one year.

Some types of livestock coal timber and domestic iron ore are also included.

Https Cdn Na Sage Com Docs En Customer Sfa 16 1 Open Fasaagd Pdf

The Ranch Mine Desert Home Desert House Desert Architect Architects Modern Architect Phoenix Arizona Son In 2020 Desert Homes Modern Architects Courtyard House

Private Villa Kuwait 500 M Sarah Sadeq Architects Modern House Exterior Bungalow House Design Facade House

Https Www Thompsonhine Com Uploads 1136 Doc Domestic Taxable Mergers And Acquisitions Pdf

Westgate Town Center Floor Plans 2 West Gate Town Center 3 Bedroom Floorplan Home Decor Bedroom Bedroom Decor Bedroom Apartment

The Evolution Of Relational Property Rights A Case Of Chinese Rural Land Reform Iowa Law Review The University Of Iowa College Of Law

Gallery Of Arundel Square Pollard Thomas Edwards Architects 1 Apartment Architecture Architect Facade Architecture

Opulence Meets Contemporary Architecture In New Delhi India E4 House Modern House Design Architecture Fancy Houses

4 61 12 Foreign Investment In Real Property Tax Act Internal Revenue Service

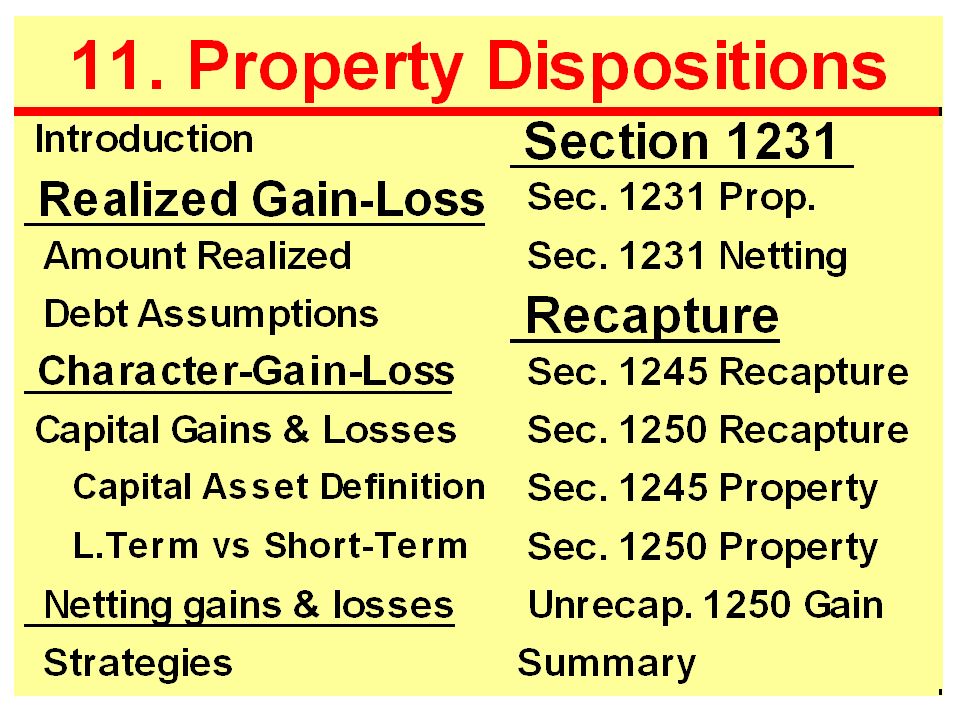

Chapter 11 Property Dispositions Howard Godfrey Ph D Ppt Video Online Download

Https Checkpointlearning Thomsonreuters Com Liveevent Download Location Prod Ecom H0191 Westlan Com Cpl Prod Marketing Webinarattachments 1369 12 29 16 20w238t Pdf Filename 12 29 16 20w238t Pdf

Section 1250 Definition

Pin By Feby Elkess On المعمارالاسلامي المعاصر Hotel Exterior House Designs Exterior Mosque Architecture