Irc Section 117

Https Www Aau Edu Sites Default Files Aau 20files Key 20issues Taxation 20 26 20finance Section 117 D Qualified Tuition Reduction Final Pdf

Https Www Irs Gov Pub Irs Wd 202009029 Pdf

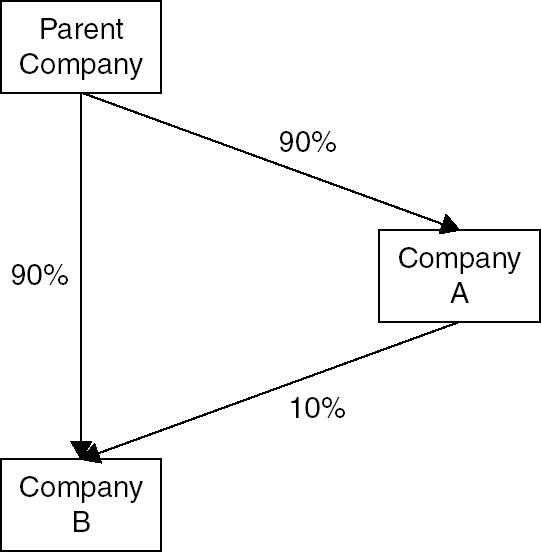

Gale Academic Onefile Document Foreign Controlled Domestic Corporations 2010

Federal Tax Benefits For Higher Education

Health At The Heart Of Prison Reform

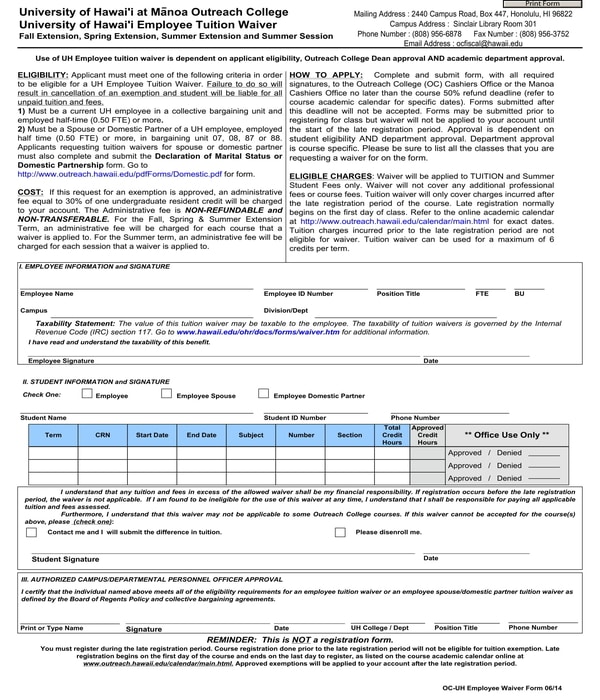

Free 12 Employee Waiver Forms In Pdf

1954 for education furnished after june 30 1985 in taxable years ending after such date.

Irc section 117. 117 b qualified scholarship for purposes of this section. Irc section 117 d irc section 132 h free or reduced tuition provided by eligible educational institutions to its employees may be excludable from gross income as a qualified tuition reduction. 117 a general rule gross income does not include any amount received as a qualified scholarship by an individual who is a candidate for a degree at an educational organization described in section 170 b 1 a ii.

Https Tax Thomsonreuters Com Content Dam Ewp M Documents Tax En Pdf Brochures Checkpoint Catalyst Topics Brochure Pdf

American Airlines Center Dallas Tx American Airlines Center Seat View Dallas Stars

What Is Included In Gross Income Ppt Download

Https Papers Ssrn Com Sol3 Delivery Cfm Abstractid 2850107

International Criminal Tribunal For The Former Yugoslavia Icty Appeals Chamber Prosecutor V Kupreskic International Legal Materials Cambridge Core

Https Core Ac Uk Download Pdf 153553013 Pdf

Chapter 7 Hvac And Ventilation Strategies Guidelines For Airport Sound Insulation Programs The National Academies Press

Surprises On Tax Treatment Of Scholarships Dennis Escoffier 2015 Journal Of Corporate Accounting Amp Finance Wiley Online Library

Definition Of A Group Chapter 5 The Taxation Of Corporate Groups Under Consolidation

Kids Save Lives Educating Schoolchildren In Cardiopulmonary Resuscitation Is A Civic Duty That Needs Support For Implementation Journal Of The American Heart Association

Nerv 10k 20181231 Htm

2

The Insolvency England And Wales Rules 2016

Https Assets Publishing Service Gov Uk Government Uploads System Uploads Attachment Data File 783976 20170922 Ukncb Faq Update To Scg Style 4 Pdf

Source : pinterest.com