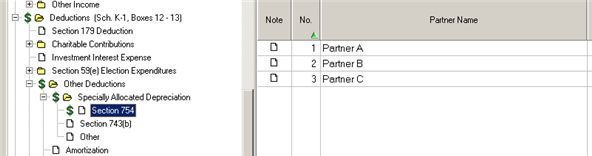

Code Section 754 Election

Https Checkpointlearning Thomsonreuters Com Liveevent Download Location Prod Ecom H0191 Westlan Com Cpl Prod Marketing Webinarattachments 1369 12 29 16 20w238t Pdf Filename 12 29 16 20w238t Pdf

9 11 Anniversary Forgotten On The Front Page Of Today S New York Times How To Memorize Things September 11 11th Anniversary

Section 754 And Basis Adjustments Pdf Free Download

Ppt Partnership Termination And Transfer Of A Partner S Interest Amanda Wilson February 21 2013 Powerpoint Presentation Id 3321120

Partnership Taxation What You Should Know About Section 754 Elections

Entering Section 754 743 B Or Other Specially All Intuit Accountants Community

1 an election under section 754 and this section to adjust the basis of partnership property under sections 734 b and 743 b with respect to a distribution of property to a partner or a transfer of an interest in a partnership shall be made in a written statement filed with the partnership return for the taxable year during which the distribution or transfer occurs.

Code section 754 election. The purpose of a section 754 election is to reconcile a new partner s outside and inside basis in the partnership. Section 754 election 1065 only under section 754 a partnership may elect to adjust the basis of partnership property when property is distributed or when a partnership interest is transferred. Such an election shall apply with respect to all distributions of property by the partnership and to all transfers of interests in the partnership during the taxable year with respect to which such election was filed and all subsequent taxable years.

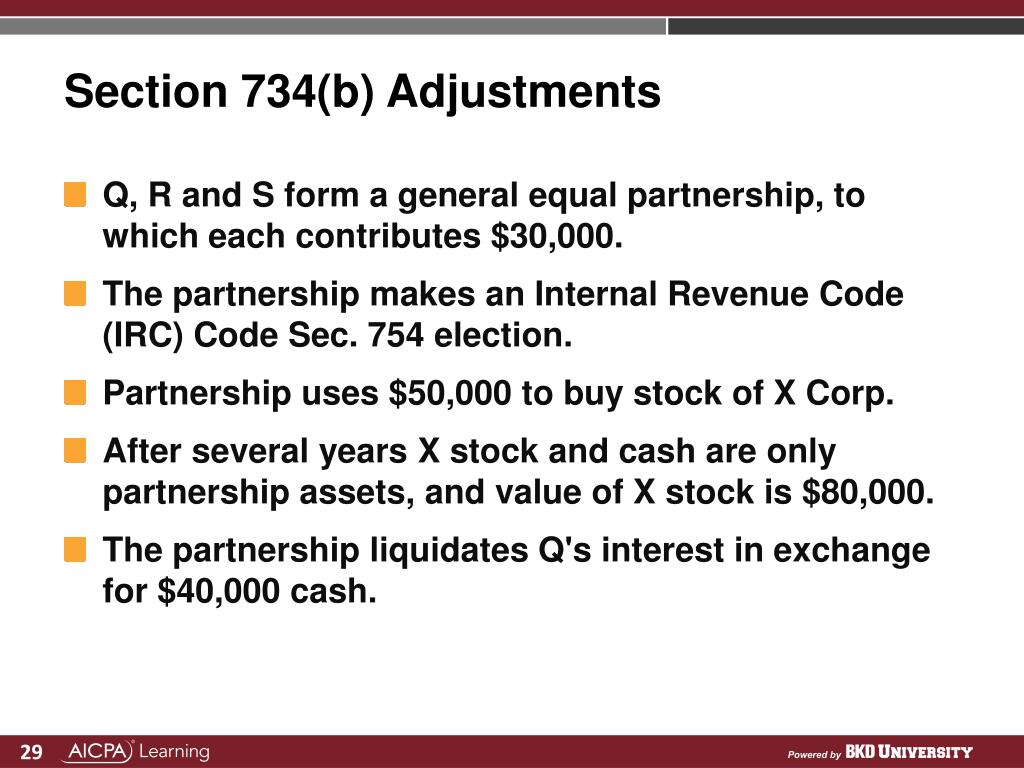

743 b 1. The company shall make the election provided for under code section 754 for the first fiscal year during which there is an exchange pursuant to section 9 1 or earlier if determined to be in the best interest of the company and its members by rhi inc. Distribution of partnership property or transfer of an interest by a partner.

Section 754 allows a partnership to make an election to step up the basis of the assets within a partnership when one of two events occurs. In the case of a transfer of an interest in a partnership by sale or exchange or upon the death of a partner a partnership with respect to which the election provided in section 754 is in effect or which has a substantial built in loss immediately after such transfer shall i r c. And such election shall not be revoked.

A section 754 election can be a favorable tax efficiency tool that is unique to partnerships as compared to corporations.

Https Www Mnd Eu Wp Content Uploads 2020 06 2019 Pdf

Section 754 What You Need To Know About Depreciation

Https Www Enterprisecommunity Org Sites Default Files Media Library Financing And Development Asset Management 2019 Tax Return Prep Guide Pdf

Https Www Oataxpro Com Assets Files Presentations Be 21 Partnership Termination On Sale Etc Pdf

Partnerships And Llc S The Basics Of Making A 754 Election Marcum Llp Accountants And Advisors

Ppt Local Government And Urban Governance Ema 754 Powerpoint Presentation Id 4362481

Jj Ker Alerte Rouge Canadien Code Barre

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcq9jukzpdvduanevj6pkauqio5won5ushutia Usqp Cau

Ppt Advanced Taxation Llcs And Partnerships Powerpoint Presentation Free Download Id 1538950

Overall Social Presence Social Webby Awards Social Media

Http Www Easywayfinder Com Map Of Florida Ormond Beach Florida Florida

Https Www Drakesoftware Com Sharedassets Manuals 2018 Partnerships Pdf

Http Ftp Pse Cz Annual Rep Tabakx012018 Pdf